POSTED BY:

COMMENTS:

0

POST DATE:

You Need Money Sharp-Sharp? A Guide to Nigerian Loan Apps

Omo, I see you. I see you for your shop, under the sun for market, for your workshop where you dey manage your tools. Things are tight. The cost of everything from fuel to garri has gone up. Sometimes, sales are slow, and you need money to restock goods. Other times, the generator knocks, or school fees for the pikin just appear from nowhere. The next thing, you are thinking, "Where can I get 20k, 50k, even 100k sharp-sharp?" My name is Segun Okonjo. I’ve spent years watching how money moves in this Lagos, from the big banks in VI to the woman selling roasted plantain in Yaba. And I know that for many of you, the bank is not an option. They will ask for your great-grandmother's birth certificate just for a small loan. So, you turn to your phone, to these loan apps that promise you money in 5 minutes. Some of them are a blessing. They can help you buy that bag of rice to resell and make a profit. But many of them? They are wolves in sheep's clothing, ready to drag your name in the mud and put you in a debt hole you can't climb out of. This guide is for you – the tailor, the mechanic, the foodstuff seller, the trader. We are going to break down these loan apps in Nigeria, so you can borrow with sense, avoid the devils among them, and use their money to grow your hustle, not to enter sapa.

Before You Borrow: 3 Crucial Questions for Nigerian Traders

Before you even download any app, stop. Breathe. Ask yourself these three critical questions. No lie, just pure truth.- Why Exactly Do I Need This Money? Is it for a real business need that will bring profit (like buying goods to sell), or is it to solve a problem that good planning could have prevented? If you are borrowing to pay back another loan, you are already in a trap. Be honest.

- How Will I Pay Back? (Be Realistic!) Don't say "God will provide." Yes, He will, but He gave you a brain to plan. Look at your daily sales. How much can you realistically set aside every day or week to pay back without starving? Write it down. If the repayment amount is more than your realistic savings, that loan is not for you.

- What If The Plan Fails? (What's Your Plan B?) What if the market is slow next week? What if the goods don't sell as fast as you hoped? Do you have a small backup? Can you call a family member for help? Going into a loan with no Plan B is like driving a car with no brakes.

Understanding Loan App Interest Rates in Nigeria

This is where they confuse and cheat people. They will say "low interest" but hide the real cost. Let's break it down in a simple way.- Daily Interest Rate: This is the devil's own cousin. An app says "1% daily interest." It sounds small, no? But 1% a day is 30% in a month! It's a trap for people who need money for a very short time, like 1-2 days. If you borrow for 30 days, you will pay a fortune.

- Monthly Interest Rate: This is easier to understand. If they say "15% per month," you know exactly what you are paying for that month. It's more transparent.

- Annual Percentage Rate (APR): The big banks use this. It tells you the total cost of the loan over one year. Most loan apps won't tell you this because the number would be frighteningly high (sometimes over 300%!).

Top 3 Trusted Loan Apps in Nigeria: A Quick Review

Let's look at some of the well-known players in the game. These are the ones that are generally more regulated and less likely to send defamatory messages to your contacts (as long as you pay on time).- Carbon (formerly Paylater): One of the oldest and most established. Acts a bit like a mini-digital bank.

- Branch: Very popular internationally and known for its simple interface and quick decisions.

- FairMoney: Markets itself as a "fair" option and is also a digital bank, offering accounts and bill payments.

Carbon Loan App Review: The "Corporate" Option

- Who it's for: People who want more than just a loan. If you like to have everything in one place (loans, savings, payments), Carbon is for you. It feels a bit more "official."

- Interest Rate: Tends to range from 5% to 15% per month, depending on your loan history with them and the loan tenure. The longer you need the money, the higher the total interest.

- Pros:

- No late fees or penalties, which is a big plus.

- The repayment schedule is flexible (weekly, monthly).

- Offers other services like bill payment and savings.

- Cons:

- The first loan amount is usually very small. You have to build trust with them.

- The approval process can sometimes be slower than others.

Branch Loan App Review: The Emergency Cash Specialist

- Who it's for: The person who needs money right now for an emergency. Their process is fast and built for speed.

- Interest Rate: Can be high, ranging from 15% to 34% monthly. The interest rate is based on their assessment of your risk from your phone data.

- Pros:

- Extremely fast. You can get money in your account in minutes.

- Very simple and easy-to-use app. No complex forms.

- They are clear about the total amount you will repay upfront.

- Cons:

- Interest rates can be one of the highest among the top players.

- Loan amounts also start small and grow slowly.

- Less flexible repayment options compared to Carbon.

FairMoney Loan App Review: Best for Market People?

- Who it's for: Traders and small business owners who also need a simple bank account. They offer free transfers and bill payments which is attractive.

- Interest Rate: Typically ranges from 10% to 30% per month. Like others, it depends on your risk profile and loan history.

- Pros:

- Gives loan offers even before you apply, based on their analysis.

- Doubles as a microfinance bank with a free bank account and debit card.

- You can get discounts on interest for early repayment.

- Cons:

- Customer service can sometimes be slow to respond.

- The app can be aggressive with repayment reminders.

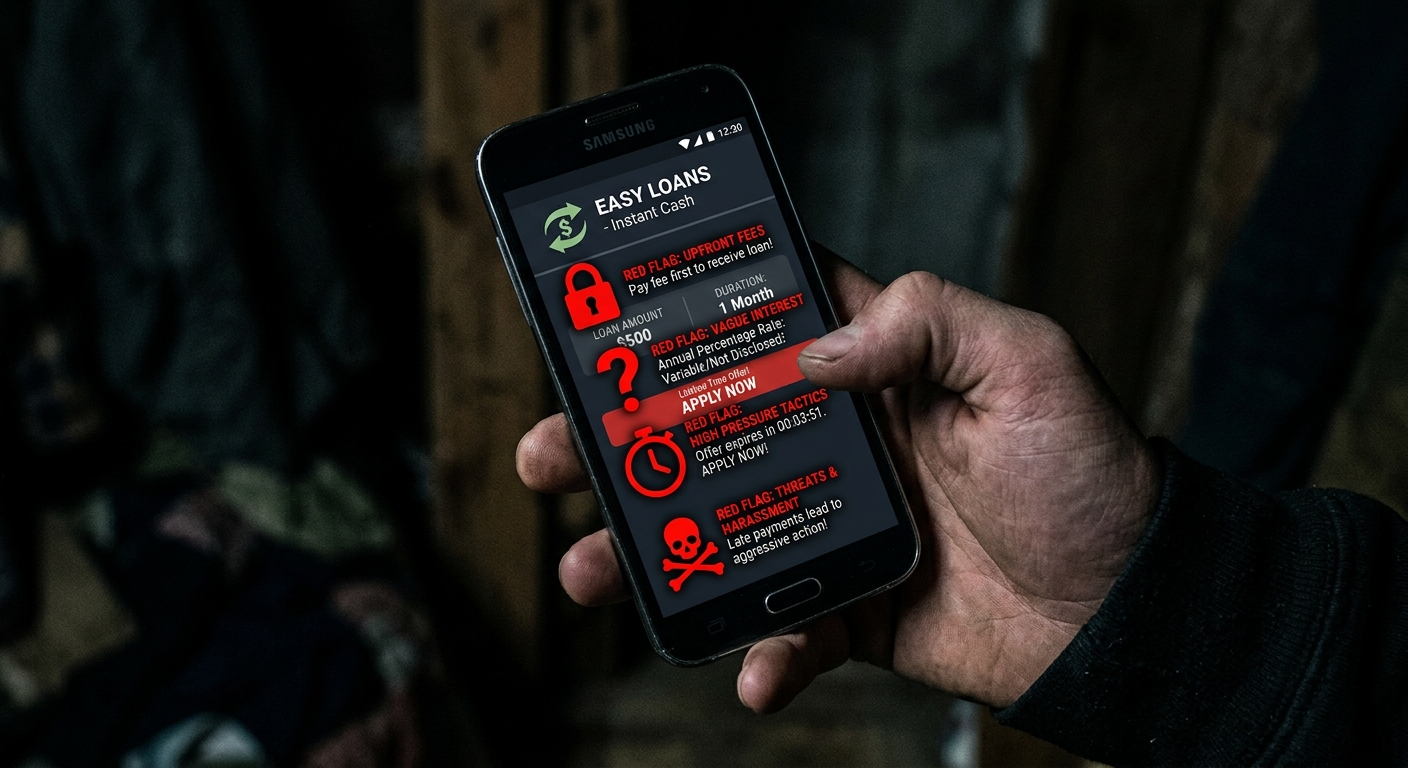

5 Red Flags: How to Spot a Fake Loan App in Nigeria

This is the most important section. Read it twice. These are signs that an app is a criminal enterprise, not a lender.

- They Ask for Upfront Fees: If any app asks you to pay a "processing fee" or "credit check fee" before they give you the loan, DELETE IT IMMEDIATELY. It's a 419 scam.

- Vague Interest Rates: If they can't tell you the exact total amount you will pay back in Naira and Kobo, run!

- Threats and Urgency: They use language like "Offer expires in 5 minutes! Apply NOW!" They are rushing you so you don't have time to think.

- No Physical Address or Full Approval: A legit lender is approved by the government. Always check the official FCCPC list of approved digital lenders before you download any app. If they are not on this list, avoid them.

- They Defame You: The biggest red flag. They threaten to send messages to all your contacts calling you a "fraudster" or "criminal" if you are one day late. This practice is illegal. Legitimate lenders use professional debt recovery processes, they don't resort to public shaming.

How Loan Apps Affect Your Credit Score

In Nigeria, we now have Credit Bureaus (like CRC Credit Bureau). Think of them as the people who keep the "book of life" for borrowers.- When you borrow from a legit app and pay back on time: The app reports your good behaviour to the credit bureau. Your "credit name" (credit score) gets stronger. The next time you need a bigger loan, maybe even from a real bank like UBA or GTB, they will see you are a reliable person and be more willing to lend to you.

- When you default or pay late: The app reports this too. Your credit name gets stained. This will make it almost impossible to get loans from any serious financial institution in the future.

Final Verdict: Carbon vs. Branch vs. FairMoney

| Feature | Carbon | Branch | FairMoney |

|---|---|---|---|

| Best For | All-in-one finance, flexible repayment | Super-fast emergency cash | Traders needing a bank account + loan |

| Interest Rate | Lower end (5% - 15% monthly) | Higher end (15% - 34% monthly) | Mid-to-high (10% - 30% monthly) |

| Speed | Moderate | Very Fast | Fast |

| Flexibility | High (no late fees, weekly options) | Low (fixed due dates) | Medium (early payment discount) |

| Killer Feature | No late fees | Speed of disbursement | Free bank account & debit card |

Beyond Quick Loans: 4 Steps to Financial Freedom

The goal is to stop needing these quick, expensive loans. They are a tool, not a lifestyle.- Separate Your Money: Get a small pouch or a separate bank account for your business. The money you make from sales is the BUSINESS'S money, not your personal ATM.

- Pay Yourself a Salary: Even if it's just N1,000 a day. Take that amount out as your own money. The rest stays with the business to buy new stock and save.

- Start a Daily "Ajo" or "Esusu": Find a trusted savings collector or just get a savings box ("kolo"). Put N500 or N1,000 inside every single day. In a month, that's N15,000 - N30,000 you saved, not borrowed.

- Know Your Profit: For every N5,000 of stock you sell, how much is pure profit? Knowing this number will help you make better decisions.