POSTED BY:

COMMENTS:

0

POST DATE:

Loan Apps vs Microfinance Banks: Which Is Better?

Listen up. Make I yan you something wey dey boil for my mind. Every day for this Lagos, I see people hustling. The woman wey dey sell roasted plantain for bus stop, the mechanic wey him hand don turn black with engine oil, the young graduate wey turn her small room to data-selling office. All of them have one thing in common: sometimes, market go slow. Sometimes, unexpected bill go show face. Sometimes, you just need that small cash injection to buy market for the next day.

Sapa is real, but the hustle is realer.

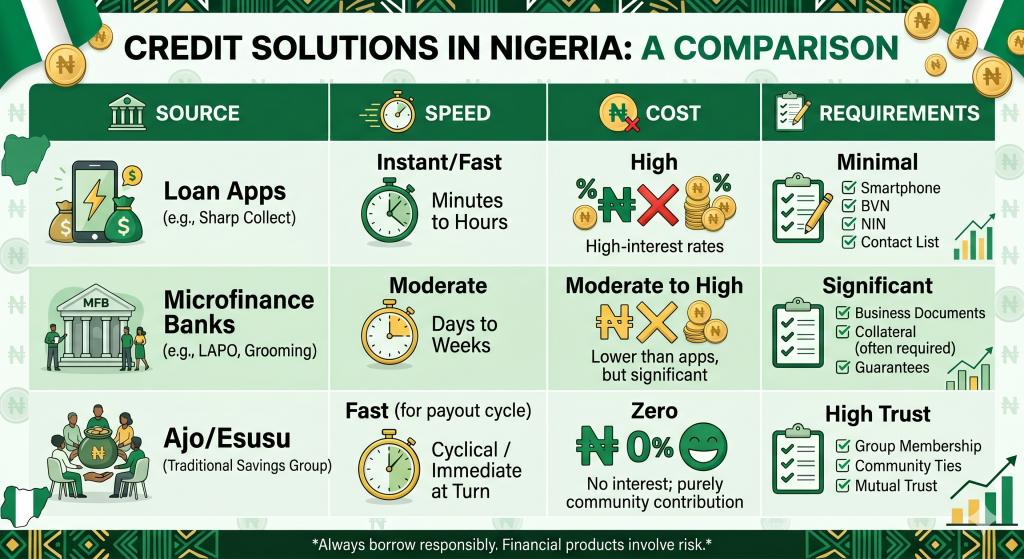

The problem no be say money no dey to borrow. The problem be say, the place you borrow from fit either build your business or bury am. You see that your small N50,000, N100,000 need? E get levels. You get the new-school digital money lenders (Loan Apps), the small-big banks (Microfinance Banks), and the old-school powerhouse wey our mama and papa use build house (Ajo/Esusu).

Today, we go put these three contenders for inside ring. We go analyse them with the brain of a Central Banker but with the language of the street. By the time we finish, you go know exactly which one fit your hustle. No guesswork.

Understanding Your Loan Options in Nigeria: The 3 Contenders

Before we start the fight, let's know our fighters properly.

- The Loan Apps: These are the new kids on the block. The sharp-sharp guys. With just your phone, BVN, and a few clicks, money fit enter your account before you finish drinking your sachet water. They are fast, they are everywhere, and they are aggressive.

- The Microfinance Banks (MFBs): These ones are like the younger brothers of the big commercial banks (GTB, Zenith, etc.). They are licensed by the CBN to serve people like you—the small business owner, the trader, the artisan. They have physical offices, proper staff, and more structured processes.

- Ajo/Esusu/Adashe (Cooperative/Thrift): This is the foundation. The original community banking. A group of trusted people (traders in the same market, workers in the same place) contribute a fixed amount of money every day, week, or month, and one person takes the full lump sum on a rotating basis. It’s built on trust, not algorithms.

Now, let the battle begin.

Digital Loan Apps in Nigeria: The Pros and Cons

These guys live inside your smartphone. They promise you heaven and earth with slogans like "Get cash in 5 minutes! No collateral! No paperwork!"

The Good:

- Speed is their superpower: This is their biggest selling point. If your generator knock engine tonight and you need money to buy parts before morning, a loan app is your fastest bet. E dey enter sharp-sharp.

- Convenience: You can apply from your bed, your shop, or inside danfo. All you need is your phone and data.

- No Collateral/Guarantor: They won’t ask you for your shop documents or your rich uncle’s phone number. Your data is their collateral.

The Bad (and the Ugly):

- Killer Interest Rates: This is where they show you pepper. Their interest is often calculated daily. A 1% daily rate looks small, but it is 365% in a year. That N20,000 loan can quickly become N35,000 if you miss your payment by a few weeks.

- Short Repayment Window: They will give you 7 days, 14 days, or maybe 30 days if you’re lucky. For a trader who needs time to turn over goods, this is serious pressure.

- The Infamous Harassment: If you default, some of the illegal ones will disgrace you. They will send messages to all your phone contacts, calling you a thief. It’s a brutal and shameful tactic. Always check if a lender is on the FCCPC's list of approved Digital Money Lenders before you even download their app.

- Data Privacy Wahala: They get access to everything on your phone. Your contacts, your pictures, everything. This is how they are able to harass you later.

Microfinance Banks (MFBs): A Better Alternative?

Think of MFBs like LAPO, Accion, or your local community bank. They are more formal than loan apps but less intimidating than the big commercial banks.

The Good:

- Reasonable Interest Rates: Their rates are much, much lower than loan apps. They are regulated, so they can’t just charge you anything they like. You are looking at rates between 3-8% per month, not per day.

- Flexible Loan Sizes & Tenors: You can get slightly bigger amounts (from N50,000 up to a few millions for groups) and you can get longer repayment periods (3 months, 6 months, even a year). This gives your business breathing space.

- They Build Your Credit History: When you borrow from an MFB and pay back on time, they report it to credit bureaus. This builds a good financial record for you, making it easier to get bigger loans in the future. Managing these repayments effectively is key, and using tools to track your business finances can make all the difference.

- Human Interaction: You can walk into their office and talk to a real person (a loan officer) who can advise you. Always confirm your MFB is licensed on the official CBN website.

The Not-so-Good:

- Not So Fast: It’s not a 5-minute game. The process can take a few days or even a week. There is paperwork involved.

- Requirements: They will ask for more than just your BVN. You’ll need a valid ID, proof of address (NEPA bill), and they might even send someone to come and see your shop or place of business. Some might ask for a guarantor.

Ajo/Esusu Contributions: The Power of Community Savings

This is the financial system of our ancestors, and it’s still incredibly powerful today. It’s banking built on one thing: trust.

The Good:

- ZERO Interest: Let me repeat that. You pay zero interest. If you contribute N5,000 every week in a group of 10 people, when it’s your turn, you collect N50,000. Not one kobo less or more. It is a forced savings plan that gives you a lump sum.

- Discipline: It forces you to save. You know that every Friday, Madam Sola will come to collect your N5,000 contribution. No excuses.

- Community Support: It’s more than just money. It’s a community. The members know you, they know your business, and they support you. There is no external harassment.

The Not-so-Good:

- It’s Slow: You cannot use Ajo for an emergency. You have to wait for your turn, which could be weeks or months away.

- The Risk of "Oga Carry Last": The biggest risk is a dishonest collector or a member who collects their money and then disappears. If the trust breaks down, the whole system collapses. You have to be very careful about the group you join.

- No Credit History: Ajo does not build your formal credit history because it’s not reported to any credit bureau. The trust is social, not financial, in the eyes of big banks.

Head-to-Head Comparison: Loan Apps vs Microfinance Banks vs Ajo

| Feature | Loan Apps | Microfinance Banks | Ajo/Esusu/Adashe |

|---|---|---|---|

| Round 1: Speed | Winner. 5-10 minutes. Unbeatable. | Slow. Days to a week. | Very Slow. You wait for your turn. |

| Round 2: Cost (Interest) | Loser. Extremely high daily/weekly rates. | Fair. Regulated monthly rates. | Winner. Zero interest. It's your own money. |

| Round 3: Repayment | High pressure. Short window (7-30 days). | Structured. Longer window (3-12 months). | No pressure. It's a savings contribution. |

| Round 4: Requirements | Minimal. BVN, phone access. | Moderate. ID, utility bill, maybe a guarantor. | Trust. You just need to be part of the group. |

The Human Factor: Customer Service vs. Community Trust

With a loan app, your customer service is an algorithm, a bot, or an aggressive agent in a call center. There is no empathy.

With a Microfinance Bank, you have a loan officer. Their job is to manage the relationship with you. They want you to succeed so you can pay back and take another loan. It’s a business relationship.

With Ajo, it’s a community relationship. These are people you see in the market every day. The trust and social pressure to not disappoint your peers is very strong.

Which Loan Option is Best for Your Nigerian Hustle?

So, which one should you choose? It’s not about which one is "best" overall, it’s about which one is "best for your current situation."

Choose a LOAN APP if:

- You have a dire emergency that cannot wait 24 hours (e.g., your delivery bike broke down and you need to fix it today to work tomorrow).

- The amount is small, and you are 110% sure you can pay it back in a few days when your customer pays you.

- My Advice: Use it like a painkiller, not like food. Use it rarely and pay it back extremely fast. Never roll over a loan app debt.

Choose a MICROFINANCE BANK if:

- You want to do planned expansion for your business (e.g., buy a new sewing machine, rent a slightly bigger shop, or buy goods in bulk for the festive season).

- You need a significant amount of money with a comfortable repayment plan.

- You want to build a formal financial history that can help you get bigger loans from big banks in the future.

- My Advice: This is the best option for serious, planned business growth. Build a relationship with one MFB.

Choose AJO/ESUSU if:

- You are not in a rush for the money and you want to build capital without paying any interest.

- You need a disciplined way to save for a specific future project (e.g., saving up to pay your shop rent for the next year).

- You are in a community where trust is high and members are reliable.

- My Advice: This is the undisputed king for interest-free capital accumulation. Every serious hustler should belong to at least one trusted Ajo group.

How to Spot Loan Scams in Nigeria

No matter where you go, shine your eye. For more information on your rights as a borrower, you can check out the CBN's financial literacy resources.

- Upfront Fees: If anyone asks you to pay a "processing fee" or "insurance fee" before you get the loan, run! It’s a scam.

- Vague Terms & Conditions: If they can't clearly tell you the interest rate, the total amount you will repay, and the exact due date, run!

- High-Pressure Tactics: If they are rushing you to sign or agree without giving you time to think, there is something they are hiding.

Frequently Asked Questions (FAQs)

1. Which loan option is the fastest in Nigeria?

Without a doubt, loan apps are the fastest. You can get money in your account within 5 to 15 minutes of applying on your smartphone. However, this speed comes at a very high cost in terms of interest rates and potential harassment. They are best for extreme, small-scale emergencies only.

2. Are Microfinance banks safer than loan apps?

Generally, yes. Licensed Microfinance Banks (MFBs) are regulated by the Central Bank of Nigeria (CBN). This means their interest rates are controlled, they follow proper procedures, and you have a formal institution to report to if there are issues. Many loan apps operate in a grey area, and while some are licensed by the FCCPC, the illegal ones can be very risky.

3. Can Ajo or Esusu help me build a credit score?

No, traditional Ajo/Esusu systems do not help you build a formal credit score. Because they are informal and based on community trust, your timely contributions are not reported to credit bureaus like CRC or FirstCentral. For building a formal credit history to get bigger bank loans later, a Microfinance Bank is the better option.

Conclusion: Your Money, Your Power, Your Choice

My people, money is a tool. The person who gives you the tool matters. A loan app gives you a hammer that is fast but can also break your hand. A microfinance bank gives you a full toolbox with instructions. An Ajo gives you the materials and helps you build the house with your own hands, brick by brick.

Don’t let desperation make the choice for you. Understand your need, weigh your options, and choose the financial partner that will respect you and your hustle. A solid system for managing collections and repayments is the foundation of a healthy business that doesn't always need to borrow.

Now you know the difference. Go and make the right choice.

Na so I see am.