POSTED BY:

COMMENTS:

0

POST DATE:

Loan Interest Rates Explained: 7 Things Must Know Before Borrowing

Why People Are Losing Money to Loan Interest Rates in Nigeria?

Alhaji Musa runs a provisions store in Kano. January comes, sales are dry, and he needs ₦50,000 to restock before the school resumption rush. He sees a loan app advertise "Only 1% daily interest!" He thinks — "1% is small, that's almost nothing." He takes the loan for 30 days.

By the time he's supposed to repay, the app is demanding ₦65,000.

He's confused. He's angry. He calls it a scam.

Here's the truth: it was not a scam. It was mathematics — and Alhaji Musa didn't understand the language being spoken to him.

1% daily × 30 days = 30% interest in one month. On ₦50,000, that's ₦15,000 extra. Gone. Into the app's pocket. Out of his restock budget.

This is the story of thousands of petty traders, market women, mechanics, and shop owners across Nigeria every single month. They borrow because they need capital to survive, but because they don't understand how loan interest rates in Nigeria actually work, they end up deeper in sapa than when they started.

Today, we fix that. No jargon. No grammar. Just real numbers and real talk that will save you money the next time you open a loan app.

The Two Languages of Loan Interest: Daily vs Monthly vs Annual Rates

Lenders in Nigeria speak interest in three different time units — and they deliberately choose whichever one sounds smallest to you. Your job is to translate everything into the same unit before comparing.

Here is the key translation table:

| Interest Type | What They Say | What It Means Per Month | What It Means Per Year |

|---|---|---|---|

| Daily Rate | 1% per day | 30% per month | 365% per year |

| Daily Rate | 0.5% per day | 15% per month | 182.5% per year |

| Monthly Rate | 10% per month | 10% per month | 120% per year |

| Monthly Rate | 5% per month | 5% per month | 60% per year |

| Annual Rate | 36% per year | 3% per month | 36% per year |

Look at this carefully. When a loan app advertises "0.5% daily," it sounds cheaper than a microfinance bank saying "10% monthly." But 0.5% daily is actually 15% per month — which is more expensive than 10% per month.

The Central Bank of Nigeria has repeatedly warned about this kind of rate presentation from unregulated digital lenders. The CBN Consumer Protection Framework technically requires transparent disclosure of Annual Percentage Rate (APR) — but enforcement in the app space remains weak, which means you must protect yourself.

The golden rule: Always convert every interest rate to "per month" before comparing two loans. If a lender refuses to tell you the monthly rate in clear terms, that refusal is your answer.

Flat Rate vs Reducing Balance: The Hidden Cost of How to Calculate Loan Interest in Nigeria

This is where even educated Nigerians lose money. There are two fundamentally different methods lenders use to calculate interest — and the same "5% monthly" can cost you 50% more depending on which method your lender uses.

Flat Rate (Simple Interest)

Interest is calculated on the full original loan amount for the entire period — even as you make repayments and your debt shrinks.

Reducing Balance (Declining Balance)

Interest is calculated only on the remaining principal you still owe after each repayment. As your balance drops, so does your interest charge.

Real Example: ₦100,000 loan at 5% monthly for 3 months

Flat Rate Calculation:

- Month 1: 5% of ₦100,000 = ₦5,000 interest

- Month 2: 5% of ₦100,000 = ₦5,000 interest (still charging on the original amount)

- Month 3: 5% of ₦100,000 = ₦5,000 interest

- Total interest paid = ₦15,000

Reducing Balance Calculation:

- Month 1: 5% of ₦100,000 = ₦5,000. You repay ₦33,333 principal + ₦5,000 = ₦38,333

- Month 2: 5% of ₦66,667 remaining = ₦3,333

- Month 3: 5% of ₦33,334 remaining = ₦1,667

- Total interest paid = ₦10,000

Same "5% monthly." One costs you ₦15,000. The other costs you ₦10,000. A ₦5,000 difference on a ₦100,000 loan — that's a full bag of rice in Oyingbo market.

Most Nigerian loan apps use flat rate. Most licensed microfinance banks officially quote reducing balance — though always confirm this directly. When any lender presents their rate, your first question is: "Is this flat rate or reducing balance?" That single question can save you thousands of naira on every single loan.

Real Street Examples: Calculate What You Will Actually Pay

Stop trusting advertisements. Start trusting arithmetic. Here are two real scenarios every Nigerian trader should study:

Scenario A: Bisi the Fabric Trader, Balogun Market, Lagos

- Loan Amount: ₦80,000

- Loan App Rate: 1.5% daily for 14 days

- Calculation: 1.5% × 14 days = 21% total interest

- Interest cost: 21% of ₦80,000 = ₦16,800

- Total repayment: ₦96,800

Bisi thought she was borrowing ₦80,000. She's actually paying back nearly ₦97,000 in just two weeks. If her profit margin from that restock is 15%, she earns ₦12,000 profit — and the loan cost her ₦16,800. She traded at a net loss to the lender. That is working for the app, not for herself.

Scenario B: Emeka the Generator Repair Man, Nnewi

- Loan Amount: ₦150,000

- Microfinance Bank Rate: 8% flat per month for 3 months

- Calculation: 8% × ₦150,000 = ₦12,000 per month

- Total interest: ₦12,000 × 3 months = ₦36,000

- Monthly repayment: (₦150,000 + ₦36,000) ÷ 3 = ₦62,000 per month

Emeka needs to confirm his repair business generates at least ₦62,000 monthly net profit above his personal expenses. If it doesn't, this loan is a trap dressed as an opportunity.

The core lesson: Calculate the final repayment amount BEFORE you collect the money. Not after. Not during. Before.

If you need help figuring out whether your business cash flow can support a specific loan repayment schedule, SharpCollect's financial tools can help you map your numbers before you commit.

The Hidden Costs Behind Daily Interest Loan Apps in Nigeria

The interest rate is the headline. The real cost is in the fine print. Nigerian lenders — especially mobile apps — are creative about stacking additional charges that never appear in the advertisement. Here is exactly what to look for:

Processing/Management Fee

Charged upfront and deducted from your loan before it hits your account. A ₦50,000 loan with a ₦2,500 processing fee means you receive only ₦47,500 in your hand — but you repay based on the full ₦50,000. Your effective interest rate just jumped before you spent a naira.

Insurance Fee

Some microfinance lenders attach "loan protection insurance" to their products. It's presented as a benefit but it's often compulsory and adds 1–3% to your total cost. Ask specifically: "Is insurance compulsory on this loan?"

Late Payment Penalties

This is the debt trap mechanism. Some apps charge 2–5% extra per day on missed repayments. Miss your date by one week? Add 14–35% more to your already-paid interest. One unexpected market problem and you're in a hole you didn't plan for.

Rollover Fees

"Extend your loan for another cycle" sounds helpful. It is not. Rolling over compounds your interest and adds new processing fees. The ₦5,000 interest you owed becomes ₦10,000–₦15,000 fast. Avoid rollovers unless you have genuinely calculated that the income coming in outweighs the additional cost.

SMS and Notification Fees

Some apps deduct small amounts for sending you repayment reminders. On short-tenure loans, these micro-deductions can add 0.5–1% to your actual cost.

How to protect yourself: Before accepting any loan disbursement, ask one specific question: "What is the TOTAL exact amount I will repay if I pay back on time, on the agreed date?" Not the rate. The total cash amount. Write it down. If they give you a range instead of a specific number, that flexibility only benefits them.

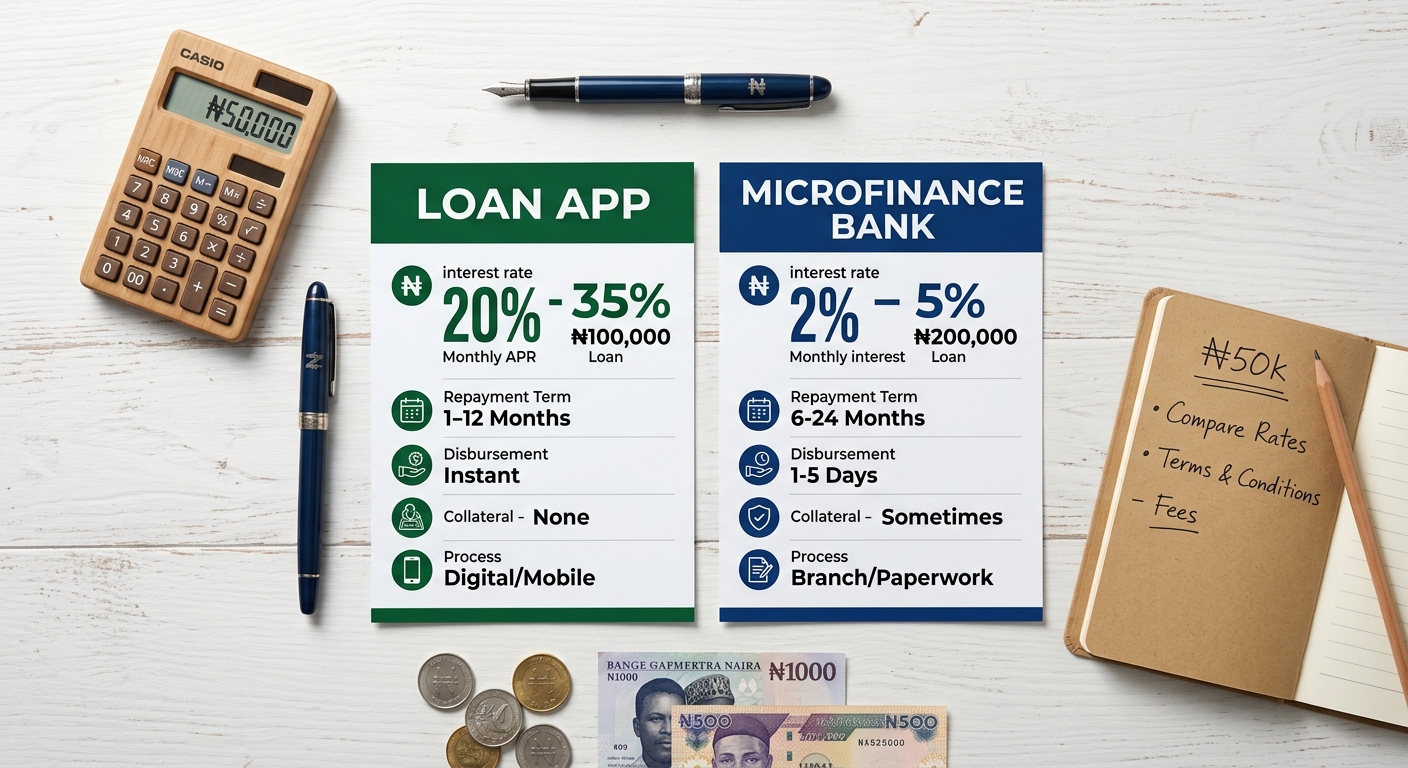

Monthly Interest Microfinance Nigeria vs Loan App Rates: The True Numbers in 2025

Let us be direct about the Nigerian lending landscape in 2025. Here is what the market actually looks like across lender types:

| Lender Type | Typical Monthly Rate (True Cost) | Processing Time | Requires Collateral? |

|---|---|---|---|

| Predatory Loan Apps (unlicensed) | 20–30%+ monthly | 5 minutes | No |

| Mid-tier Digital Lenders | 10–15% monthly | Same day | No |

| CBN-Licensed Loan Apps | 5–10% monthly | Same day | No |

| Microfinance Banks (informal products) | 5–8% monthly | 1–3 days | Sometimes guarantor |

| Cooperative Society Loans | 2–5% monthly | 3–7 days | Member guarantee |

| Ajo/Esusu Group Loans | 0–2% monthly | When it's your turn | Social trust |

The most expensive money in Nigeria is convenience money. The faster and easier a loan is to get, the higher the true cost. This is not coincidence — it is the business model.

That does not mean fast loans are always wrong. Sometimes your Idumota market restock cannot wait five days. But you must price the convenience honestly into your decision. A 25% monthly interest loan funding stock that earns you 12% monthly profit is not capital deployment — it is a slow haemorrhage.

For a comparison of which specific apps are currently CBN-licensed versus operating in grey zones, the FCCPC's list of approved digital lenders is the authoritative source. Check it before downloading any new loan app.

How to Find the Cheapest Loan in Nigeria: 4-Step Comparison Framework

Here is a clean 4-step framework. Run every loan through this before you accept a single kobo.

Step 1: Convert to the Same Time Unit

Take both rates and convert to monthly. Daily rate × 30 = monthly. Annual rate ÷ 12 = monthly. Now you are comparing the same currency.

Step 2: Identify the Rate Type

Flat or reducing balance? If it's flat, the true cost versus a reducing balance loan at the same stated rate is approximately 40–50% more expensive in actual cash paid. If they won't tell you the method, assume flat and price accordingly.

Step 3: Add Every Fee

Processing fee + insurance + any other confirmed deduction. Add these to the total interest. Divide the entire extra amount by your loan principal to get the true cost percentage.

Step 4: Calculate Your Monthly Cash Outflow

How much naira leaves your hand every single month for this loan? Can your business support that outflow AND still cover your family's feeding, rent, and operational costs? If the answer is "no" or "I'm not sure" — do not take that loan. Uncertainty is not a repayment plan.

Understanding this framework is part of building a clean credit profile that works for you long-term. At SharpCollect, tools exist specifically to help Nigerian SMEs track their borrowing history and make smarter credit decisions over time.

Red Flag Phrases in Nigerian Loan Advertising That Signal Danger

When a lender or an app uses these phrases, your suspicion level should immediately increase:

- "No interest!" — There is always a cost. It is hiding in fees, mandatory insurance, or inflated processing deductions. Free money does not exist in Nigerian fintech.

- "Just 1%!" — 1% of what? Per what time period? This incomplete sentence is specifically designed to bypass your critical thinking. Always finish the sentence yourself.

- "We will manage the repayment for you" — This means automatic direct debit or wallet deductions, often with timing and amounts you don't control. Read every permission you grant this app.

- "Rollover available" — Convenient language for a compounding debt trap. Rollovers benefit lenders, almost never borrowers.

- "Your BVN is our collateral" — This is a harassment warning, not a financial arrangement. It means they will contact your family members, employer, and phone contacts if you miss a payment. The FCCPC has banned this practice for licensed lenders, but many apps still do it.

- "Limited offer, collect now" — Real financial products don't disappear in 24 hours. Artificial urgency is a sales manipulation tactic designed to stop you from thinking clearly. Think clearly anyway.

Your Simple 3-Step Interest Check Before Every Loan in Nigeria

Memorise this framework. Run it every time, without exception.

Step 1: Ask the "What Will I Repay?" Question

Before accepting disbursement, ask the lender directly: "If I borrow ₦X and repay on time, what is the exact total amount I will pay back?" Calculate the same number yourself using the methods in this article. If the numbers don't match what they tell you, something is hidden in the gap.

Step 2: Divide the Extra Cost by Your Expected Profit

(Total Repayment – Loan Amount) ÷ Expected Profit from the Investment = Loan Cost as % of Your Profit

If this number exceeds 50% — meaning the loan is consuming more than half your expected profit — the loan is not working for you. You are working for the loan. That reversal is how small traders stay small.

Step 3: Name Your Repayment Source Before You Touch the Money

Know the specific day money is coming in. Know which exact sale, customer payment, or market day funds your repayment. Name it before you collect. "Something will come" is not a repayment plan — it is a wish. Wishes don't protect your BVN.

Borrow Sharp, Not Blind: Final Word on Loan Interest Rates in Nigeria

Interest rates are not the enemy. Ignorance about loan interest rates in Nigeria is the enemy.

The same loan that destroys Mama Ngozi's provisions business can work profitably for a trader who understands the true cost, builds it into their pricing, and holds a specific repayment plan. The difference between those two outcomes is not luck, connections, or starting capital. The difference is knowledge.

Credit has always been part of the Nigerian hustle. Ajo, esusu, cooperative loans — our grandmothers understood informal credit long before fintech existed. The apps and microfinance banks have not changed the fundamental principle: money borrowed must earn more than it costs. That rule is eternal.

So before the next time you open a loan app at midnight because sales have been dry and you need to restock before morning:

- Convert the rate to monthly

- Ask for the total repayment amount in exact naira

- Check if your expected profit covers the cost with margin to spare

- Name your repayment source before you collect

If those four things check out — take the money and move sharp-sharp.

Your financial literacy is the most powerful business tool you own. It costs nothing to learn, requires no collateral, and cannot be repossessed. But it will save you tens of thousands of naira every single year — and over a decade of trading, that difference is the gap between a shop and a warehouse.

Borrow smart. Repay on time. Build your credit history one clean loan at a time.

Segun Okonjo is a veteran fintech analyst and financial literacy advocate based in Lagos. This content is for educational purposes to help everyday Nigerian workers make smarter borrowing decisions.

Frequently Asked Questions About Loan Interest Rates in Nigeria

What is the average loan interest rate in Nigeria for small traders in 2025?

The average loan interest rate in Nigeria varies significantly by lender type. CBN-licensed loan apps typically charge 5–10% per month, microfinance banks charge 5–8% per month on flat rate products, while unlicensed or predatory apps can charge 20–30% per month or more. Cooperative societies remain the cheapest option at 2–5% monthly. Always convert any advertised rate to a monthly figure before comparing, and confirm whether the lender is using flat rate or reducing balance calculation, as the same stated percentage can cost you 40–50% more under a flat rate structure.

How do I calculate loan interest on a Nigerian loan app?

To calculate loan interest on a Nigerian loan app, follow these three steps: First, identify whether the rate is daily, monthly, or annual, and convert it to monthly (multiply daily rate by 30, or divide annual rate by 12). Second, confirm whether the calculation method is flat rate or reducing balance — most apps use flat rate, which means interest is charged on the original loan amount throughout the entire tenure. Third, multiply the monthly rate by the number of months, then multiply that percentage by your loan principal. Add any processing fees, insurance charges, or other deductions to get the true total repayment amount. Always ask the lender for the specific total repayment figure in naira before accepting any disbursement.

Which loan is cheapest in Nigeria for petty traders without collateral?

For petty traders without collateral, the cheapest loan options in Nigeria in 2025 are: Ajo or Esusu cooperative groups (0–2% monthly, but require group membership and patience), registered cooperative society loans (2–5% monthly, require being an existing member), and CBN-licensed microfinance bank products (5–8% monthly, require guarantor in some cases). Among instant digital lenders that require no collateral whatsoever, CBN-licensed loan apps with transparent rate disclosure are the safest and most affordable option, typically ranging from 5–10% monthly. Before downloading any loan app, verify its licensing status on the FCCPC's approved digital lenders register to avoid predatory lenders that charge 20–30% or more per month.